# Reward curve with capped issuance

There is a paradigm for the design of the reward curve, with similar economic effects as the reward curve with tempered issuance, at least with the setting that will be highlighted here. The paradigm is to adopt a reward curve with capped issuance, that replicates the current reward up to some cap, defined by the deposit size at which issuance stops growing $D_c$. Since this policy is rather similar to the reward curve with tempered issuance, the reader is encouraged to review its associated [ethresearch post](https://ethresear.ch/t/reward-curve-with-tempered-issuance-eip-research-post/19171) that goes into great detail on various trade-offs for the design. My write-up on the [foundations of minimum viable issuance](https://notes.ethereum.org/@anderselowsson/Foundations-of-MVI) from yesterday might also be useful.

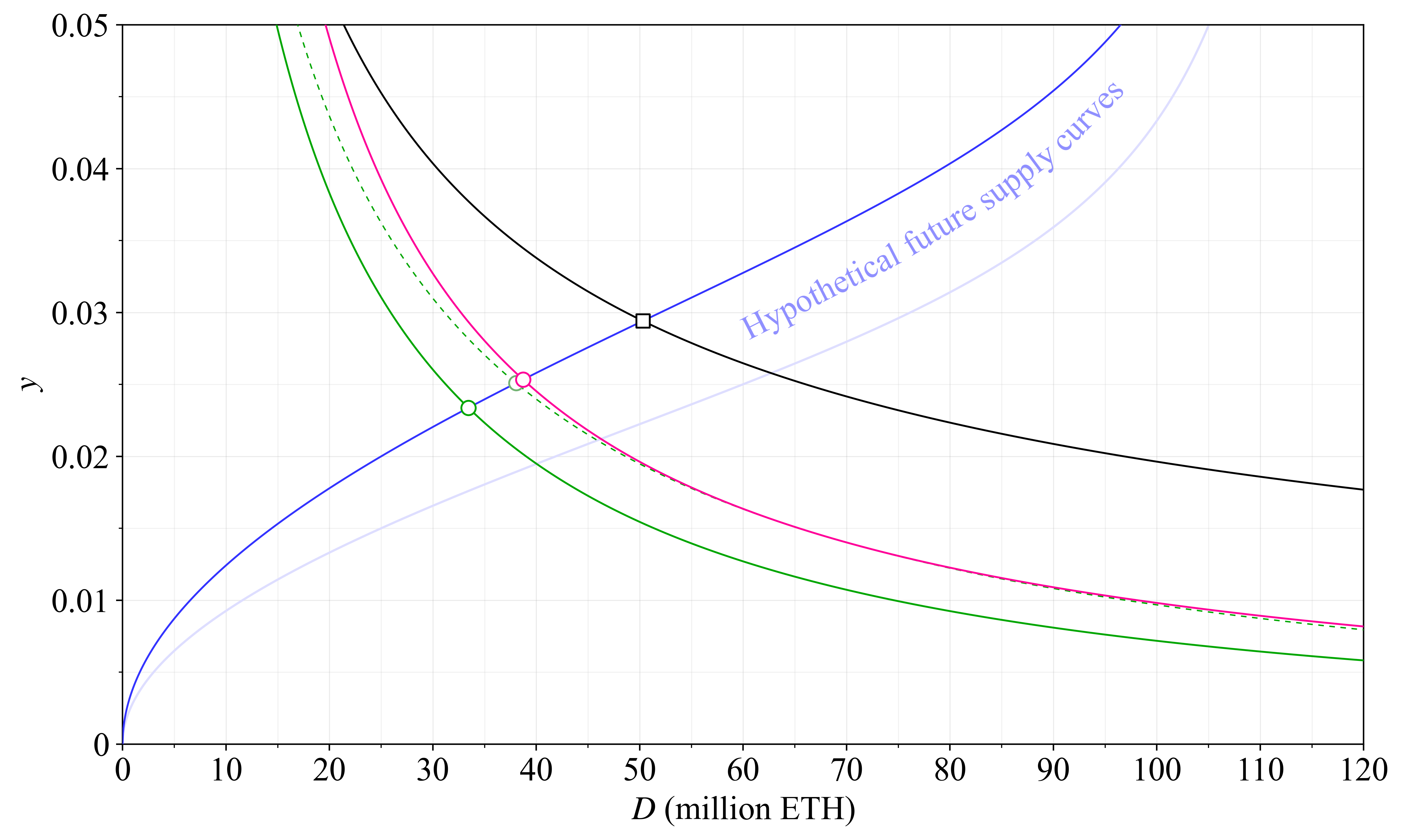

The figure below illustrates a reward curve in pink where the cap kicks in at $D_c=2^{24}$. One interesting detail is that Vitalik's [active validator cap and rotation proposal](https://ethresear.ch/t/simplified-active-validator-cap-and-rotation-proposal/9022) from 2021 has the same effect on issuance as when using the setting of $D_c=2^{24}$. The green reward curves are alternatives with tempered issuance specified in [Section 3.1](https://ethresear.ch/t/reward-curve-with-tempered-issuance-eip-research-post/19171#h-31-option-a-proposed-reward-curve-13) of the previously linked write-up. As evident, the reward curve with an issuance cap would also halve issuance relative to the current trajectory at $D=2^{26}$, just as the tempered issuance under a graduated approach. Of course, it might seem appealing to stakers to then cap issuance at the current deposit size instead, i.e., $D_c=2^{25}$. However, the gains from adopting such a policy would be much more limited, albeit not insignificant. In my view, a change to $D_c=2^{24}$ is then clearly preferable in the case that a change is instituted using this paradigm.

The figure below instead shows the effect on staking yield under the current level of MEV (300 000 ETH/year). Hypothetical future supply curves are illustrated in blue (discussed in the longer previous write-up).

I will return shortly with a longer write-up on this paradigm, detailing its benefits and drawbacks, and most interesting variants. One of those is extensions using methods described in [Section 6.3](https://ethresear.ch/t/reward-curve-with-tempered-issuance-eip-research-post/19171#h-63-the-unknown-endgame-39). Just as with the reward curve with tempered issuance, the reward curve with capped issuance is trivial to implement. One interesting question is if the simplicity of this design makes it easier to accept to the community. The reward curve with tempered issuance is of course also very simple in its design: divide the equation for the current reward curve by $1+D/k$. But it might not "look" as simple. An aspect that can both be a benefit and drawback is the discontinuity and specific shape around the cap, which will be discussed further in the forthcoming longer write-up.